Institutional Insights: Goldman Sachs 'Dollar & Commodity Volatility'

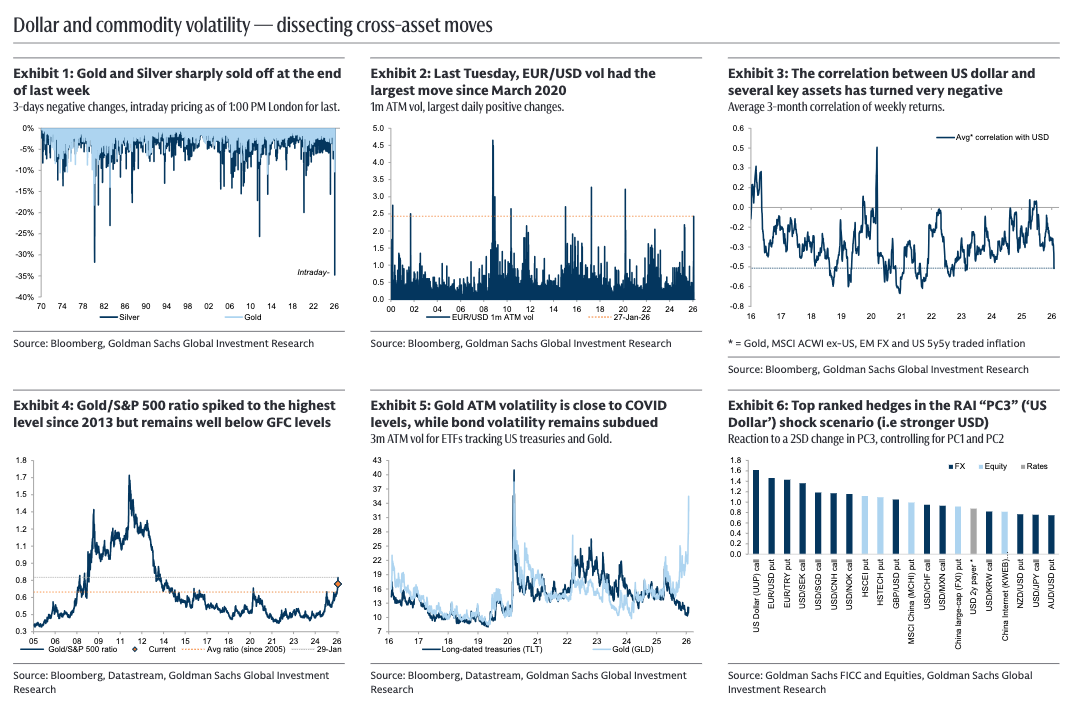

Last week experienced significant movements across various assets, especially in precious metals. Gold and Silver saw sharp corrections, with Gold dropping 11% and Silver plummeting by 31%, marking their steepest declines since the 1980s (Exhibit 1). The S&P 500 briefly touched 7,000 on Wednesday during the release of 4Q25 earnings, where 47% of market capitalization reported, and 59% exceeded consensus EPS by more than one standard deviation. The Dollar hit its lowest level since February 2022 but rebounded later in the week. The Federal Reserve held interest rates steady at 3.50–3.75%, citing improved growth and labor market conditions, while Kevin Warsh was nominated as the next Fed Chair.

The ISM Manufacturing Index released today came in strong at 52.6, surpassing the median forecast of 48.5. Attention this week shifts to policy decisions from the ECB and the BoE. Meanwhile, our Risk Appetite Indicator (RAI) surged to five-year highs two weeks ago, driven by growth optimism (RAI PC1, Exhibit 14). However, the RAI has since moderated as momentum in key drivers—such as small-cap stocks, cyclicals, emerging market assets, and Dollar weakness—has begun to fade. Notably, EUR/USD broke above 1.20 on Tuesday, marking the largest daily volatility increase since March 2020, before retreating in recent days (Exhibit 2).

The weaker US Dollar has been a significant driver of risk appetite year-to-date (Exhibit 14). Cross-asset correlations indicate that multiple assets have shown a negative correlation with the currency (Exhibit 3), particularly global equities outside the US, with emerging market (EM) equities, EM currencies, and commodities like gold standing out. Geopolitical tensions have further fueled upward pressure on commodities, with precious metals experiencing sharp rallies. This was amplified by a liquidity squeeze in London, driving the Gold/S&P 500 ratio higher, even as equities hit new all-time highs (Exhibit 4). Short-term gold volatility has risen since Q4 2025, spiking to levels not seen since the COVID-19 crisis during Friday’s selloff (Exhibit 5). Meanwhile, rates volatility remains subdued, despite policy uncertainty being repriced through tighter swap spreads and steeper yield curves.

Looking ahead to 2026, we maintain a modestly pro-risk stance in our asset allocation, acknowledging that heightened risk appetite could lead to increased market volatility. Our FX team forecasts a modest decline in the US Dollar this year, with more pronounced weakness against EM and cyclical currencies. However, while rate differentials may have a limited impact, factors such as policy uncertainty and institutional governance concerns are likely to play a more significant role. To address US asset dominance, we are actively pursuing regional diversification across various assets and implementing selective FX hedging strategies, such as tight call/put spreads. Our commodities team maintains a baseline projection of reaching $5,400 by December 2026. In the event of a rising Dollar shock scenario (as indicated by our PC3 ‘US$’ declining), appealing option strategies include Dollar (UUP) calls and EUR/USD puts (refer to Exhibit 6).

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!